With the launch of various electronic banking channels, the use of paper-based banking instruments have declined by at least 28 percent, both in the number and value of transactions.

Records with the Royal Monetary Authority (RMA) show a steady growth in the volume of overall payment instruments in the third quarter of 2019 on all modes of instruments, including paper-based, mobile and internet, electronic, card, and wallet.

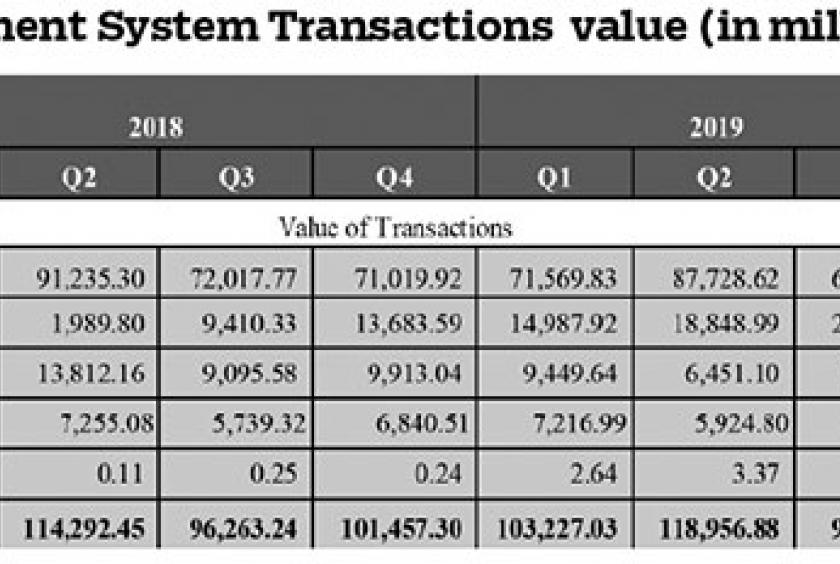

The volume of paper-based transactions dropped from 328,270 in the second quarter to 237,030 transactions in the third quarter. In terms of monetary value, paper-based instrument declined to Nu 62.4B from Nu 87.7B during the same period.

The volume of overall payment system transactions in the third quarter, ending 30 September 2019, saw an increase of 37 percent compared with the previous quarter. The second quarter saw almost 9M transactions as compared to more than 12M transactions in the third quarter.

Mobile and internet recorded the highest number of transactions, 7.7M in the third quarter and its share to the total payment system is 63 percent during the quarter. However, in terms of value, its share is only 21 percent when compared to paper based, 63 percent. This is because most of the transactions that are huge in amount, especially those initiated by government and corporate bodies are paid in cheque.

“Based on the average value of each transactions processed using the cheques (260,555 cheques), it is observed that cheques are mostly used for making large value fund transfer,” the RMA stated in its quarterly report.

In terms of percentage increase, card transaction recorded the highest increase in the value and volume of transaction, which was contributed by increase in the ATM withdrawal using domestic as well as Rupay cards. Card involves transactions made through ATM, PoS and RuPay.

RuPay, according to the RMA has been picking up since its launch in the previous quarter, which contributed to the overall increase in card transaction.

Both the value and volume of transactions done through mobile app and internet show an increasing trend.

In the third quarter, the volume of transactions increased by 14 percent to 7.7 million, while the value increased by 11 percent to Nu 20.99B as compared to the second quarter of 2019. The average value of each transaction is Nu 2.73, which means mobile and internet payment channels are mostly used for making small value retail payments.

During the quarter, banks exited the operation of National Electronic Clearing System (NECS) and National Electronic Funds Transfer System (NEFT) with effect from October 2019.

The GIFT system replaced the NECS and NEFT as a platform to make retail payments and interbank fund transfer during the third quarter. The GIFT system offers three payment components such as BULK, BITS, and RTGS to effectively make retail payments, interbank fund transfer, and also real time large value fund transfer respectively.

In terms of volume, BULK has the highest percentage share in all quarters from amongst the three transfer channels, whereas, RTGS dominates the share for value since it facilitates all the large value fund transfers.